Holiday Apartments on Gold Coast

Josh Stewart

Investing in a Gold Coast holiday apartment offers a vibrant lifestyle and potential financial benefits, but requires careful consideration and planning.

Understanding Australian Property Trends

Josh Stewart

The Australian property market is diverse, with varying trends in growth between houses and units across capital cities.

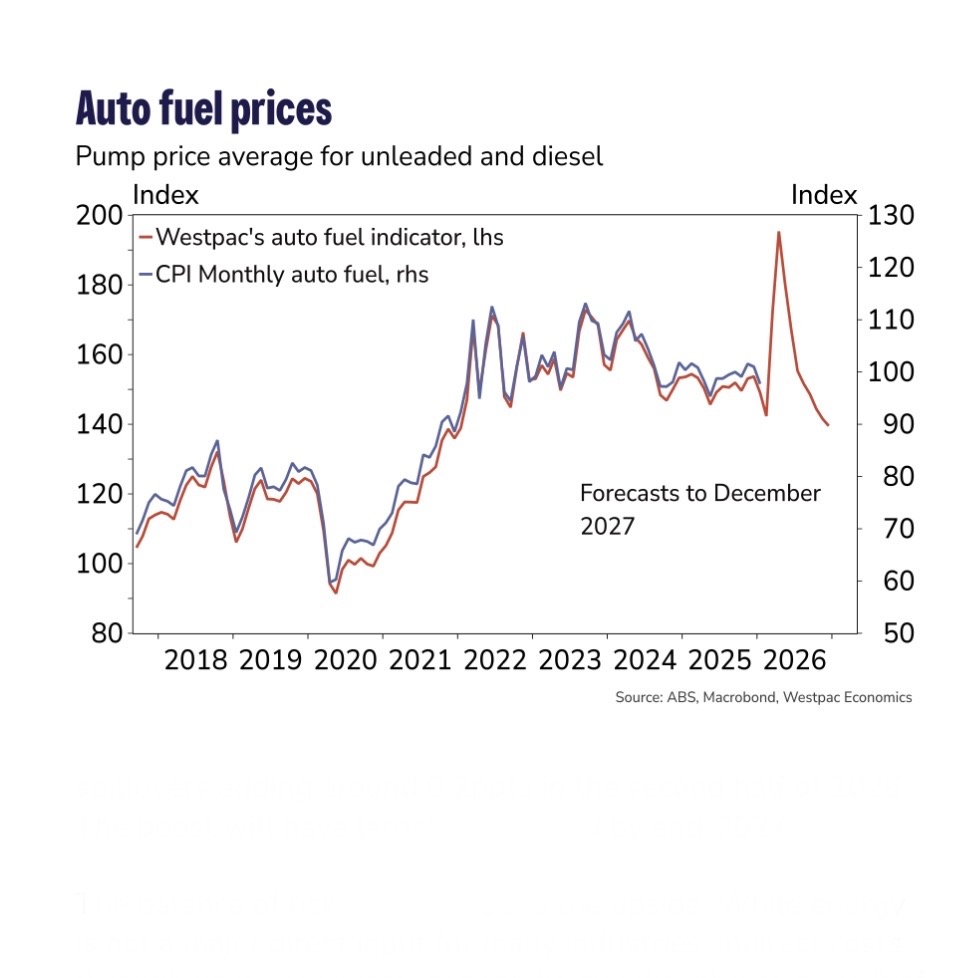

Aussie Fuel Price Trends

Josh Stewart

Fuel prices in Australia fluctuate due to global events, affecting consumers and requiring savvy shopping for the best deals.

Australia's Rising Borrowing Costs

Josh Stewart

Australia's borrowing costs have surged, impacting homeowners and investors, with rates forecasted to remain high until 2025.

Australia's Inflation Journey Overview

Josh Stewart

Australia's inflation peaked in early 2023 but has been steadily declining toward a more manageable rate, with projections complicating the recovery.

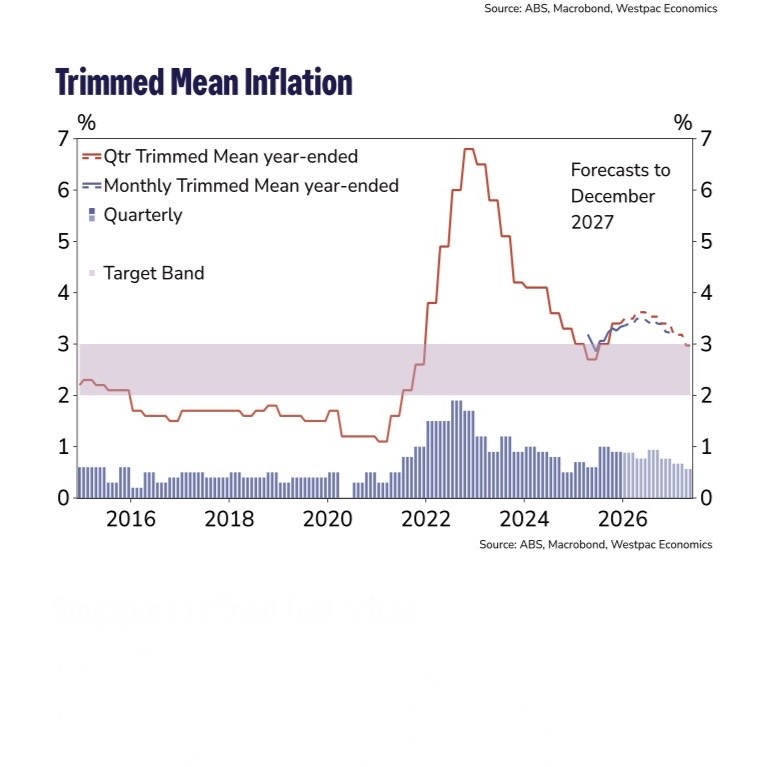

Understanding Trimmed Mean Inflation

Josh Stewart

Trimmed mean inflation in Australia provides a clearer view of underlying trends, indicating easing inflation and economic stability ahead.

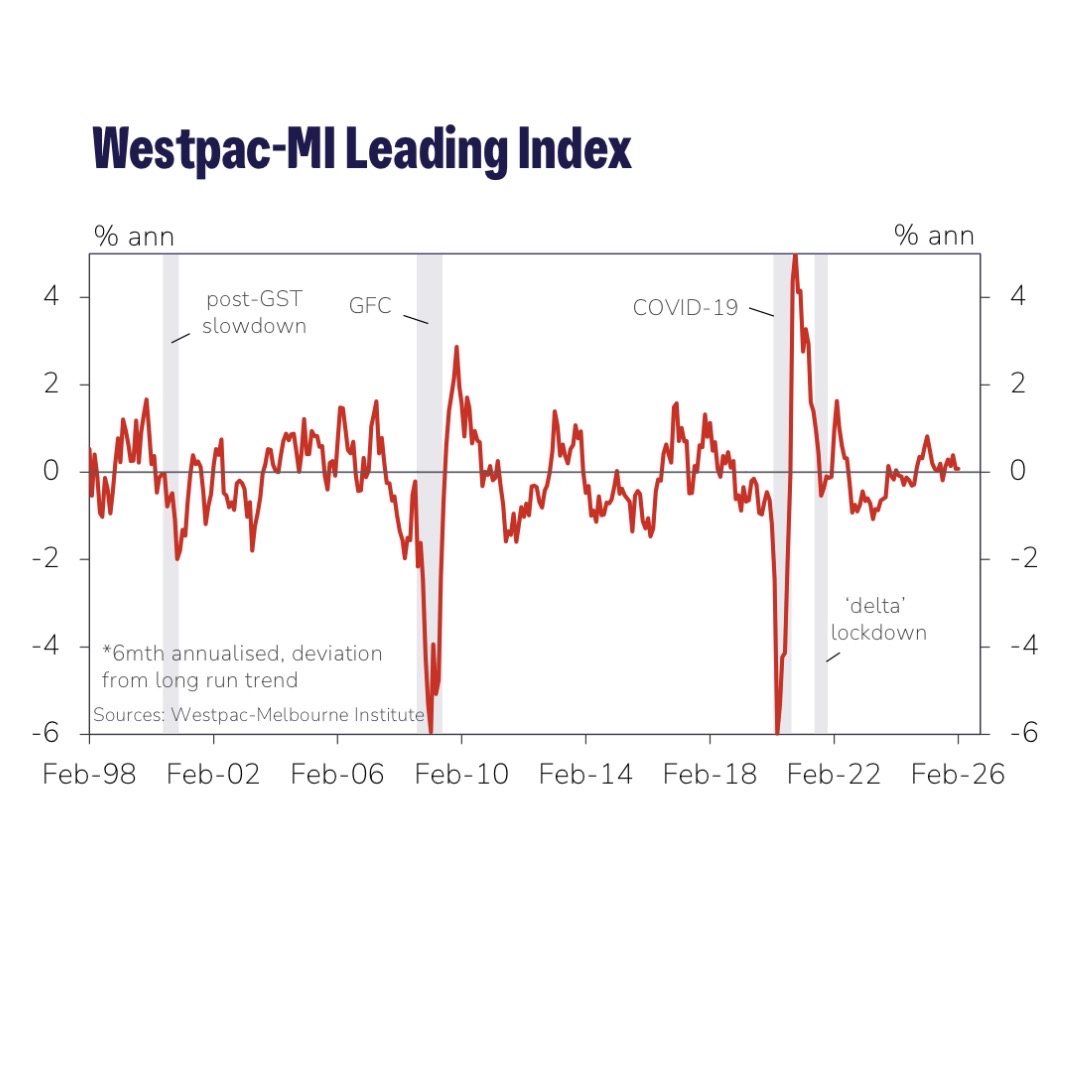

Westpac-MI Leading Index Insights

Josh Stewart

The Westpac-MI Leading Index forecasts cautious economic growth in Australia, influenced by consumer sentiment and interest rate changes.

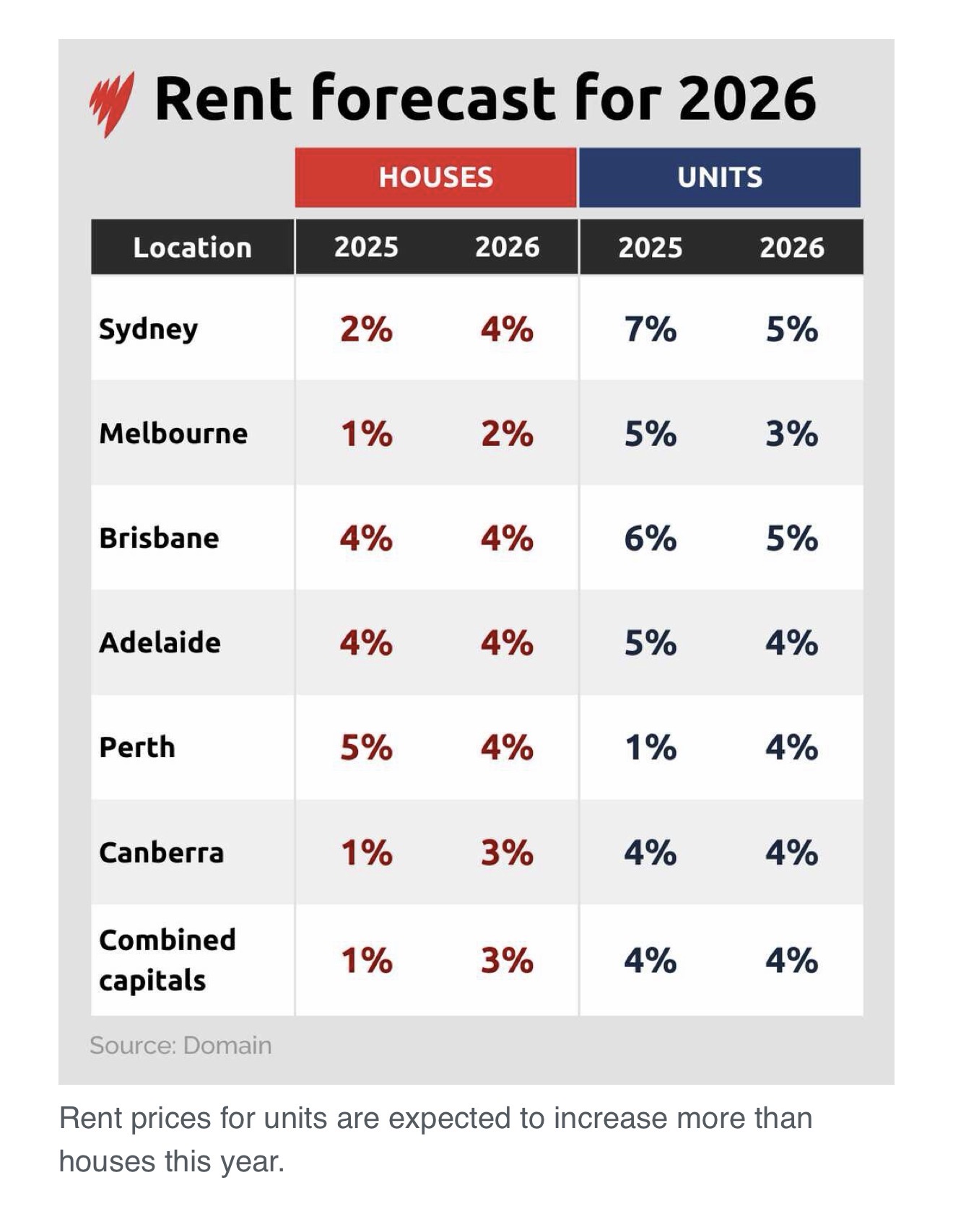

Australian Rental Market Forecast 2026

Josh Stewart

Forecasts for the Australian rental market in 2026 indicate varying growth rates across cities, with units generally outperforming houses.

Australia's 2026 Property Forecast

Josh Stewart

Australia's 2026 property price forecast indicates steady growth, with varied trends across major cities and a slight dip in Canberra.

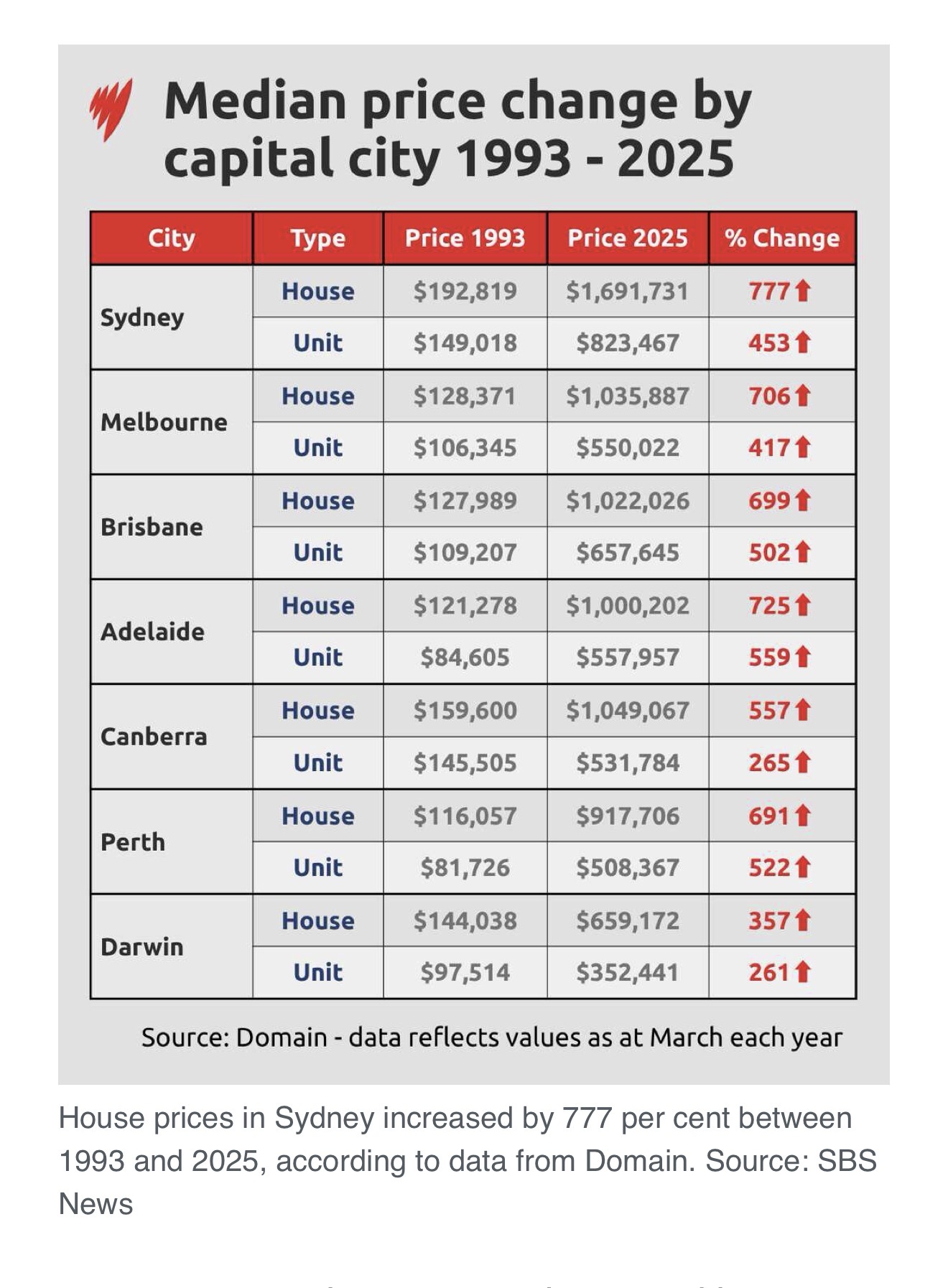

Australian Property Price Growth

Josh Stewart

Australian property prices have significantly increased since 1993, with Sydney experiencing a remarkable 777% rise by 2025.

Wages vs Housing Affordability

Josh Stewart

Despite wage growth in Australia, soaring housing costs have undermined financial stability and homeownership for many citizens.

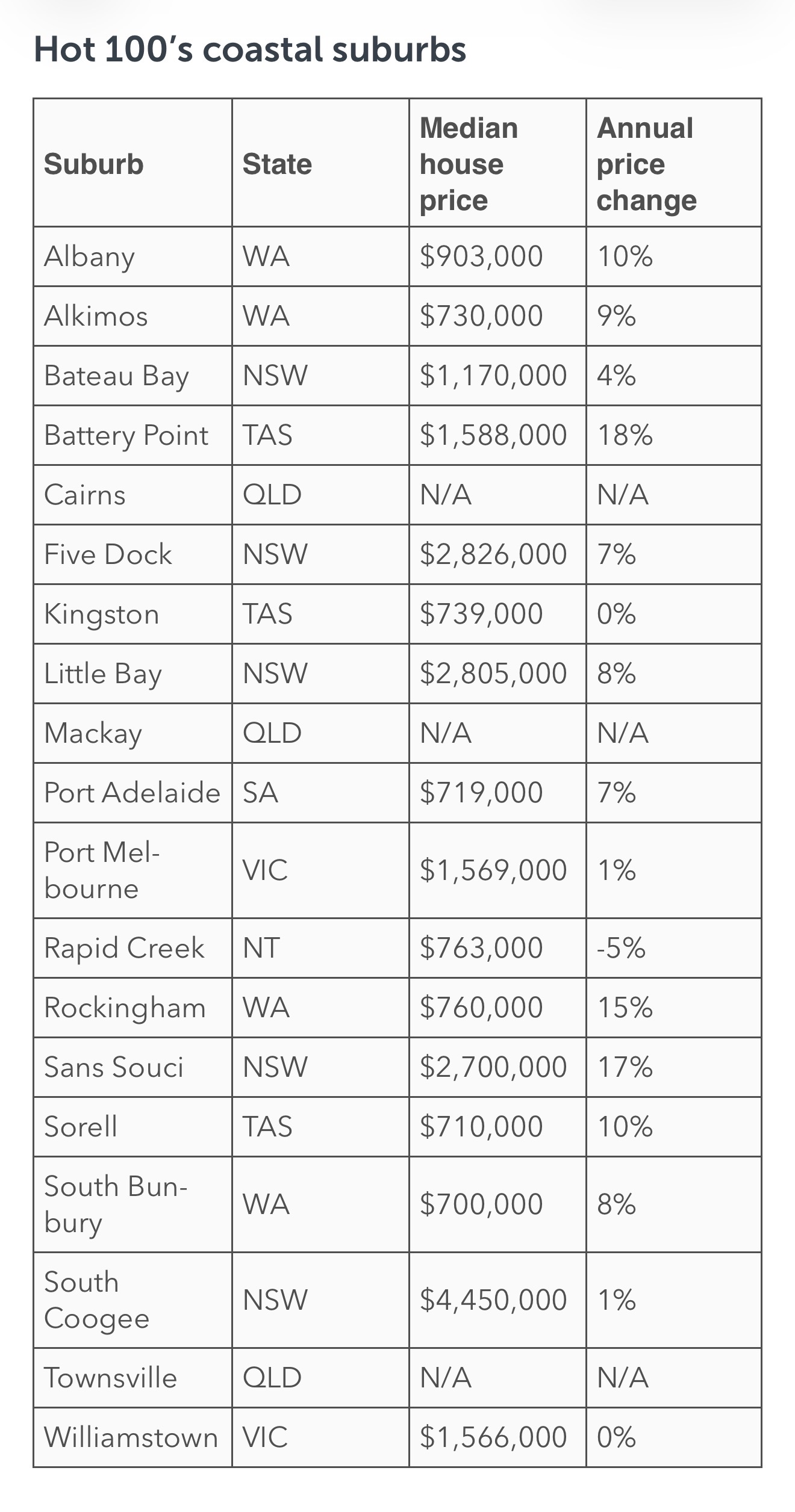

Australia's Coastal Property Insights

Josh Stewart

Australia's coastal property market shows robust growth and diversity, with significant price increases in several regions despite some stability and declines elsewhere.

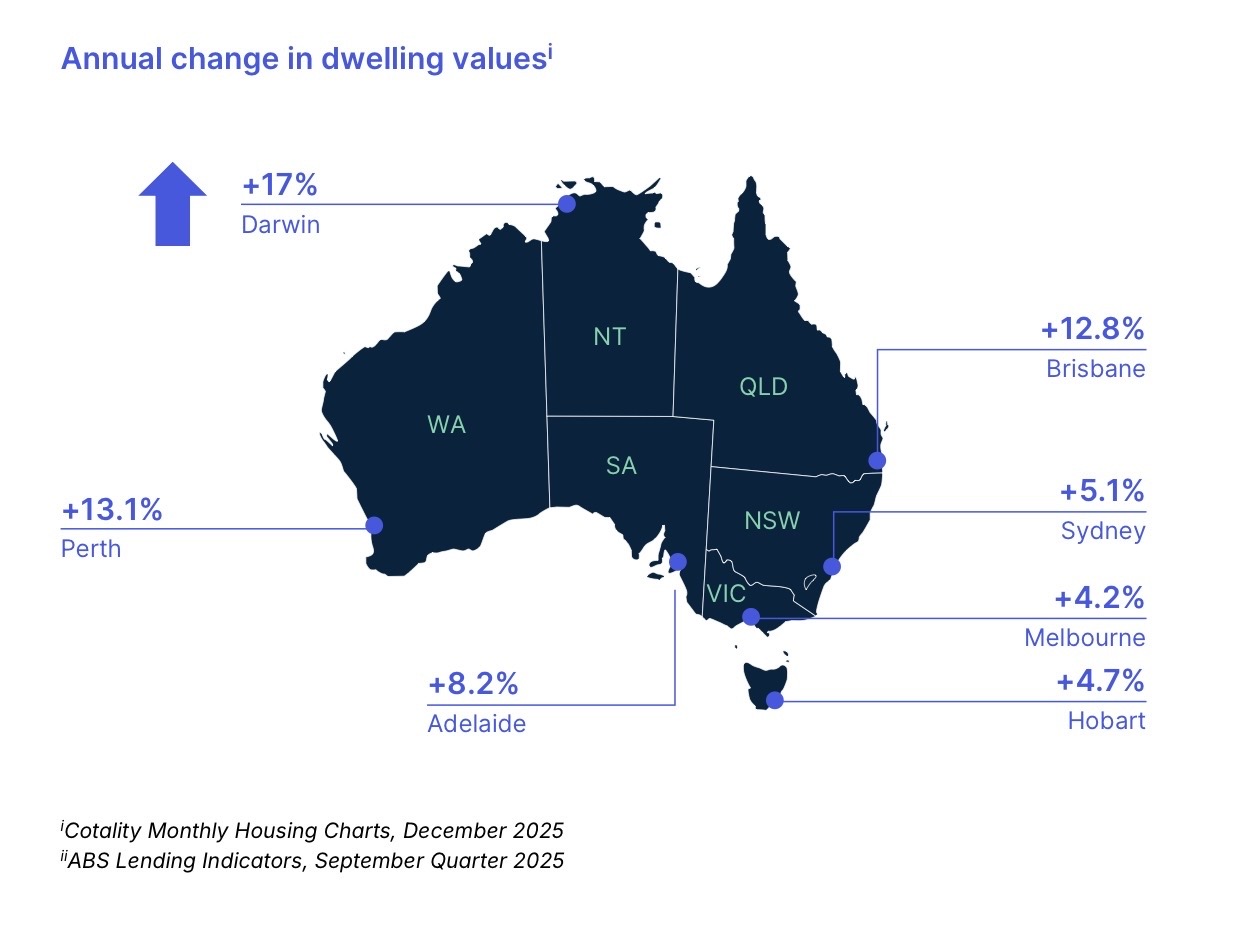

Australia's Property Market Trends

Josh Stewart

Australia's property market saw significant growth in 2025, with Darwin leading at a 17% increase in dwelling values.

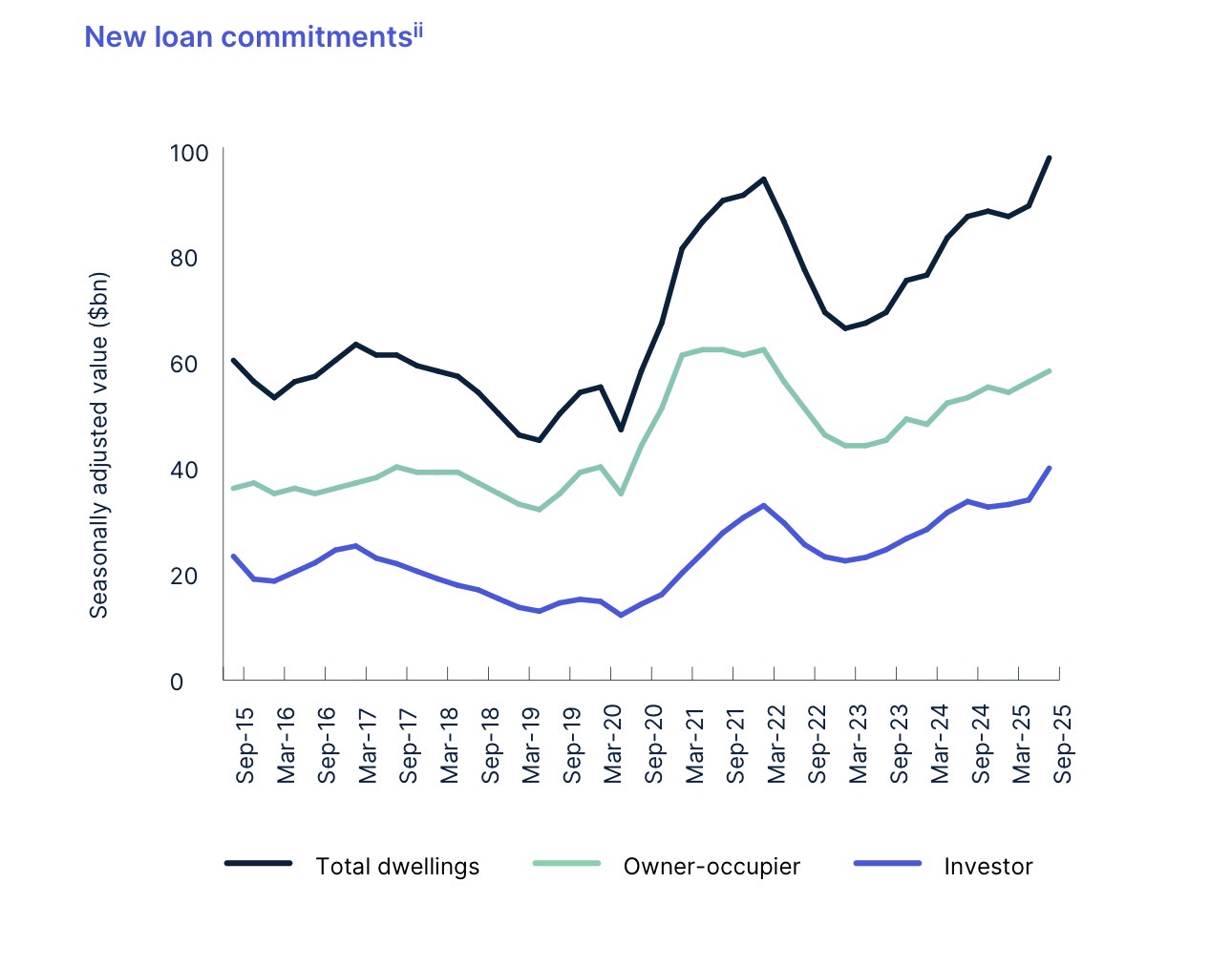

Australia's Housing Market Trends

Josh Stewart

Australia's housing market is experiencing significant growth driven by robust demand and a chronic supply shortage amid rising loan commitments.

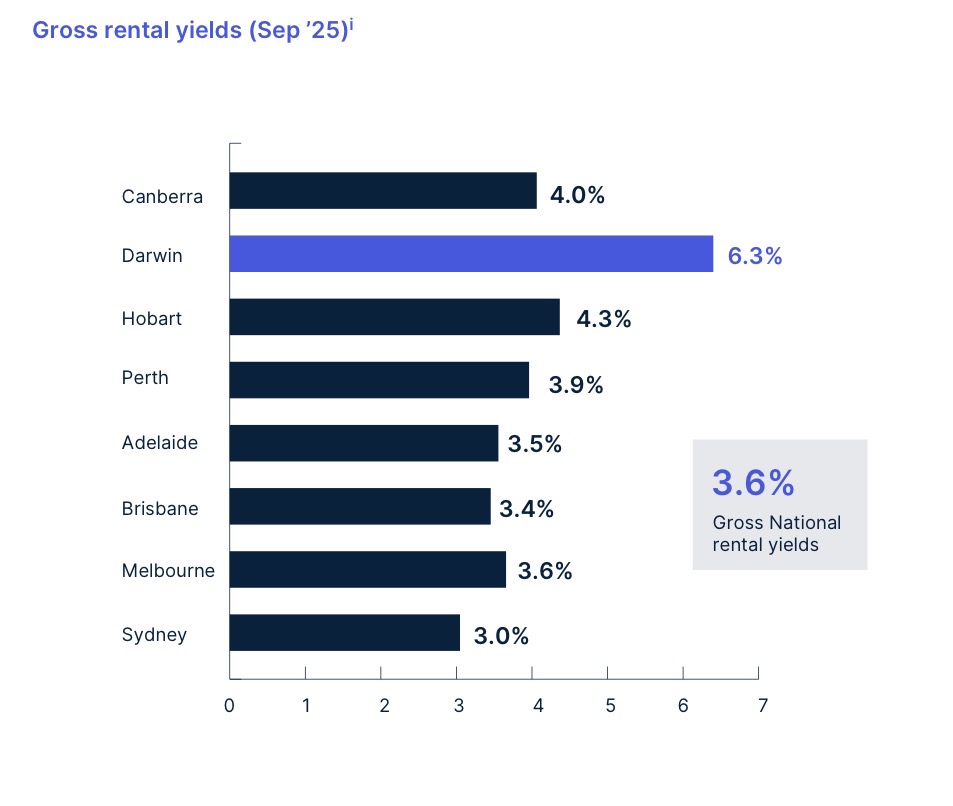

Best Rental Returns in Australia

Josh Stewart

Australia's rental market shows Darwin leading with 6.3% yields, while Sydney and Melbourne offer lower returns and potential capital growth.

Australian Housing Market Trends

Josh Stewart

The Australian housing market is characterized by cyclical highs and lows, with recent data indicating a possible recovery by mid-2025.

Australia's New Office Developments

Josh Stewart

Australia is experiencing a surge in new office construction, reflecting confidence in physical workplaces despite trends toward remote work.

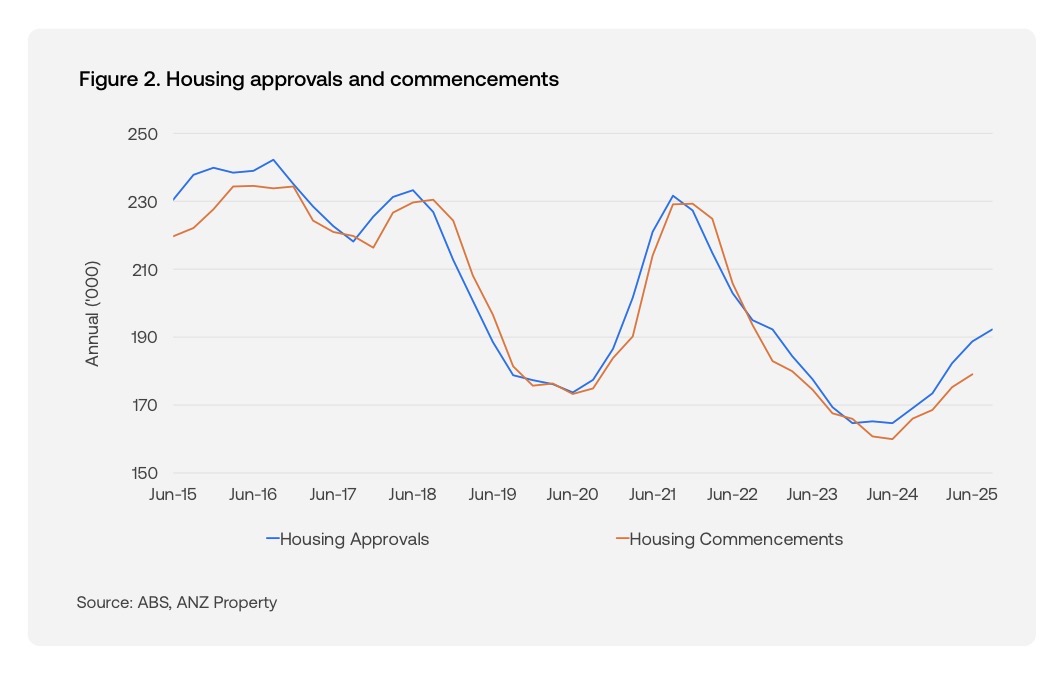

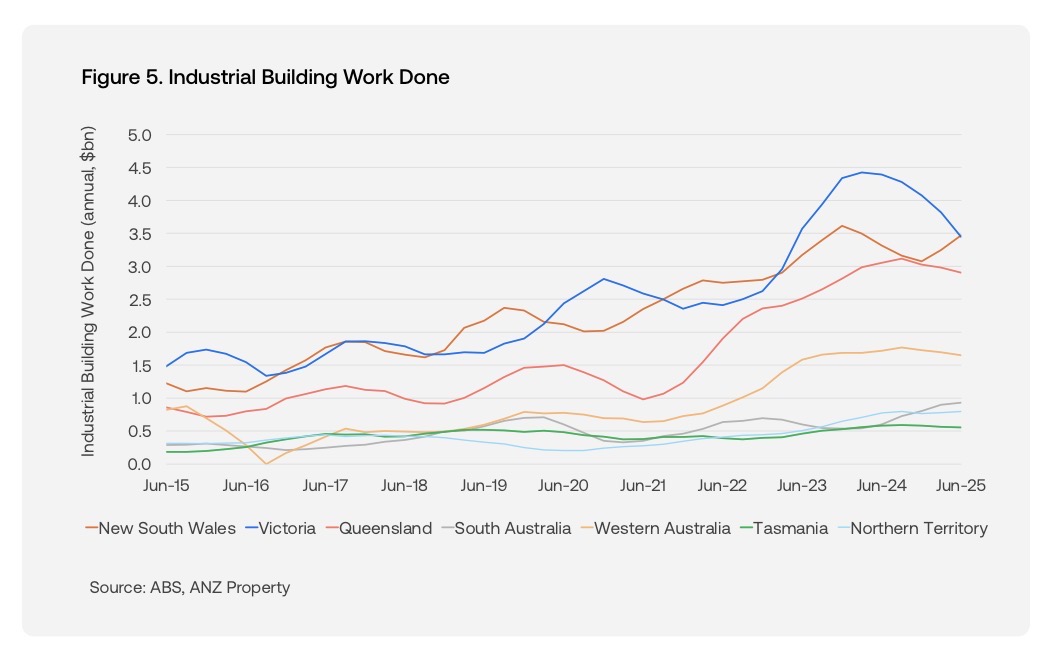

Australia's Industrial Building Growth

Josh Stewart

Australia's industrial building sector shows significant growth variations across states, with Victoria's peak followed by a predicted decline.

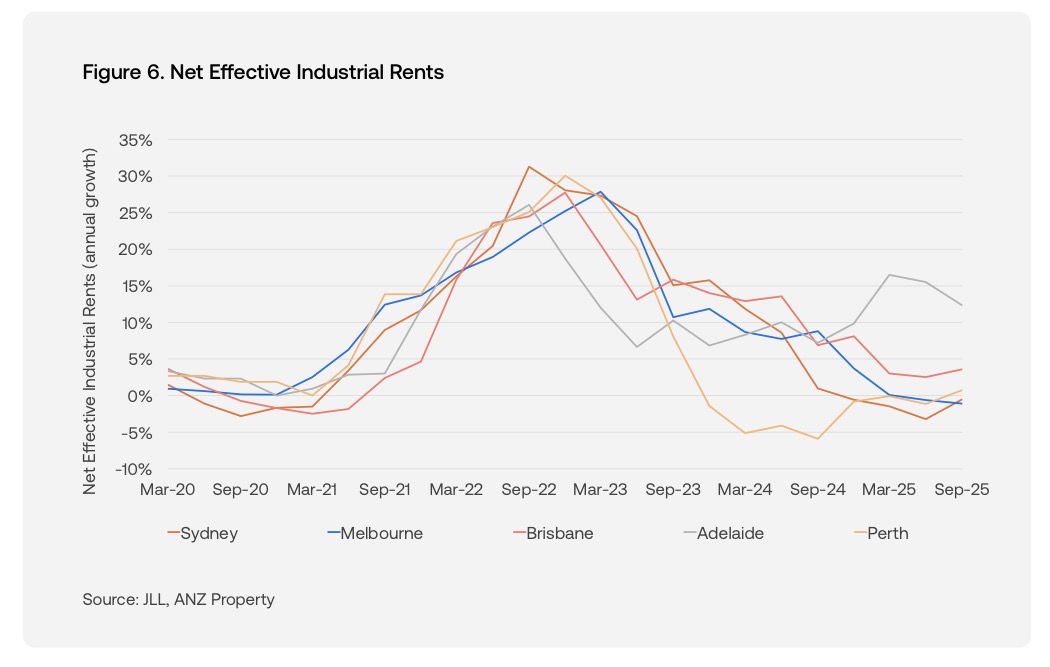

Australia's Industrial Rental Market Trends

Josh Stewart

Australia's industrial rental market has experienced significant fluctuations, with recent trends indicating a stabilization and potential growth in specific cities.

Generational Wealth Distribution Trends

Josh Stewart

The wealth gap narrows as Gen X surpasses Boomers in property wealth, amid a significant intergenerational wealth transfer.

Rental Property Ownership in Australia

Josh Stewart

Most rental properties in Australia are owned by individuals with just one property, not large corporations or wealthy investors.

Impact of Scrapping Negative Gearing

Josh Stewart

Removing negative gearing may harm the economy, reducing GDP, construction jobs, and increasing rental prices.

Surge in Property Investor Activity

Josh Stewart

Investor activity in the Australian property market is surging, reshaping trends and creating new opportunities distinct from owner-occupiers.

Housing Market and CGT Changes

Josh Stewart

Proposed changes to Australia's Capital Gains Tax could negatively impact housing supply, GDP, and rental prices, sparking nationwide concern.

Financial Future Navigation Guide

Josh Stewart

Navigating your financial future requires a clear plan, regular reviews, and strategic goal-setting to ensure stability and growth.

Business Wellness Programs Overview

Josh Stewart

Cultivate a healthy workplace culture to boost productivity, collaboration, and overall business success.

Understanding Interest Rate Increases

Josh Stewart

Interest rate hikes will increase borrowing costs, impacting borrowers while benefiting savers; preparation is essential to navigate these changes.

Impact of Interest Rate Hikes

Josh Stewart

Rising interest rates significantly impact monthly home loan repayments, highlighting the need for homeowners to budget and prepare accordingly.

Understanding Home Building Costs

Josh Stewart

Building a new home in Australia involves rising costs, careful budgeting, and strategic planning for a successful outcome.